Real GDP forecast (%)

| 2019 | 2020E | 2021E | |

|---|---|---|---|

| World | 2.8 | -4.1 | 4.9 |

| U.S. | 2.2 | -4.3 | 3.1 |

| Eurozone | 1.3 | -7.6 | 4.8 |

| Japan | 0.7 | -5.5 | 2.7 |

| China | 6.1 | 1.5 | 7.5 |

| ASEAN | 4.2 | -3.8 | 5.3 |

Global economic growth is expected to rebound in 2021, but not without bumps along the way.

Accommodative monetary policy, as well as fiscal stimulus should lend support to growth.

Key risks include a worsening pandemic, escalation of U.S.-China tensions and an upsurge in emerging market flashpoints stemming from pandemic-related catalysts.

The global economy is crawling out of the depths to which it had plummeted during the nationwide lockdowns. Many economies are gradually recovering with the help of decisive actions taken by major central banks and governments. We expect global economic growth to improve from a low base, with global GDP growth forecast at 4.9% in 2021.

Still, the path to full recovery may not be smooth. Some countries have recently slowed reopening and/or reinstated partial lockdowns following a resurgence in COVID-19 cases. COVID-19 will remain a threat until an effective treatment or vaccine becomes widely available, which could be in the second half of 2021.

Read MoreAmong the major economies, China is expected to spearhead this growth at 7.5%. Meanwhile, U.S. economic growth is expected to recover to 3.1% in 2021, underpinned by consumption as well as fiscal stimulus. In contrast, we are less sanguine on Europe and Japan’s economic recovery and believe they may take even longer to return to pre-COVID-19 levels.

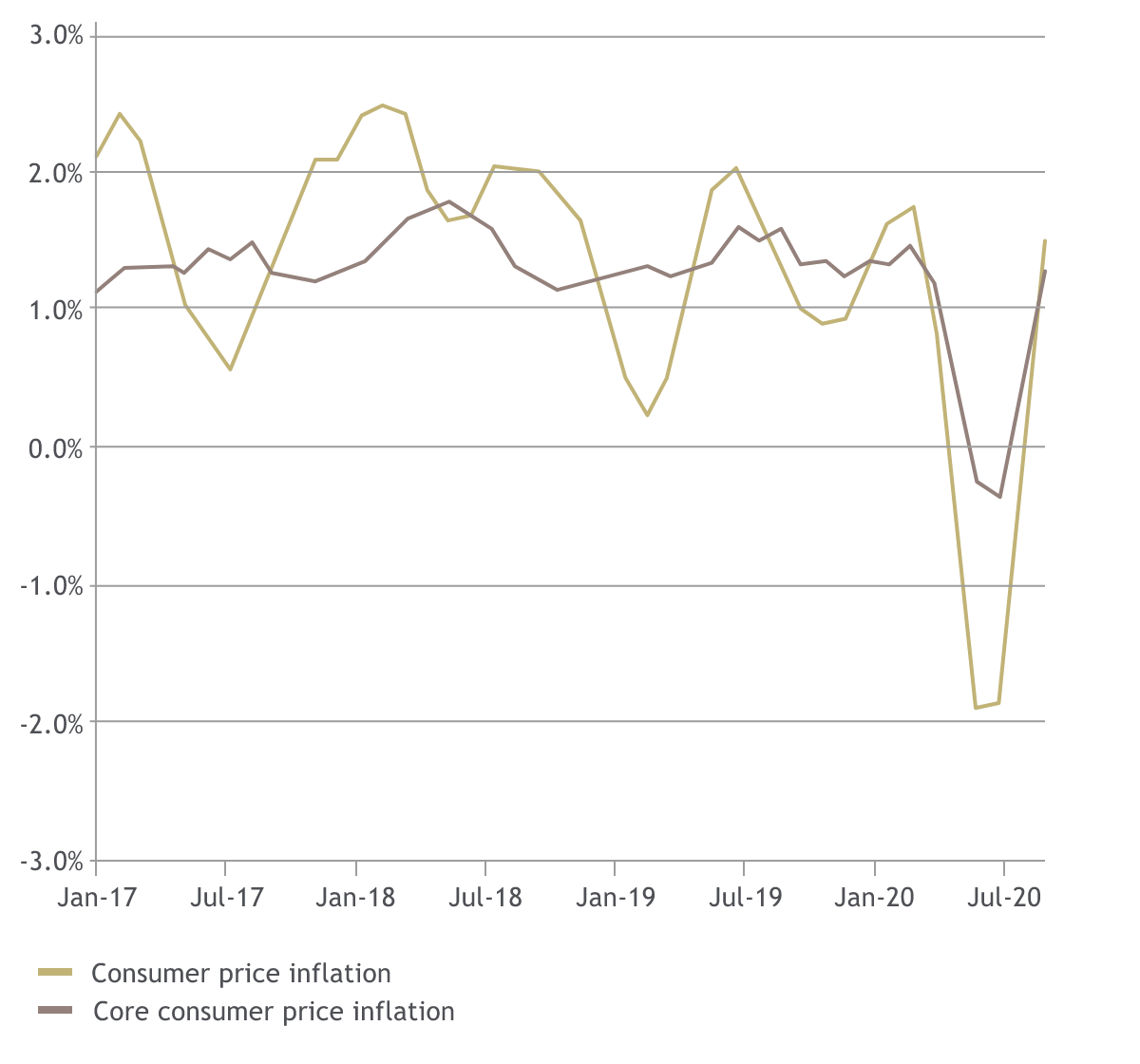

Inflation has remained largely muted, particularly in the developed world, since the global financial crisis. Not surprisingly, inflation fell again due to the impact of COVID-19, although it is likely to tick higher in 2021 as economic activities gradually recover. Despite the upside pressures, the still soft job market, as well as wage growth, will likely limit the rise in inflation. Consequently, global central banks will likely be able to maintain an easy monetary policy stance.

Specifically for the U.S., as part of unprecedented actions taken to stabilise the economy at the onset of the COVID-19 crisis, the U.S. Federal Reserve (Fed) took the Fed Funds Rate back to all-time lows, where it is expected to remain for at least the next three years. In addition, a slew of emergency measures such as unlimited asset purchases and credit/loan facilities to buy certain corporate bonds, asset-backed securities and commercial paper were introduced very quickly.

Some of these measures are set to continue into 2021 and keep short-term U.S. Treasury (UST) yields anchored in the near term. Longer-term bond yields could however grind higher given our expectation of a gradual economic recovery.

On the fiscal front, Joe Biden’s victory with a potential split in control of the Congress (i.e. Democrat House and Republican Senate) may constrain the ability of the new U.S. administration to implement massive fiscal stimulus. Nevertheless, we believe both parties will eventually agree on a stimulus deal, albeit on a more modest level. In addition, we see a reduced likelihood of higher taxes and tighter regulations for selected sectors such as technology, especially given the immediate growth challenges.

Read MoreSimilar to the Fed, the European Central Bank (ECB) also implemented a EUR 1.85 trillion Pandemic Emergency Purchase Programme (PEPP) to fund asset purchases of both private and public sector securities. The PEPP was scheduled to expire in March 2022 but could be further expanded and extended should there be significant setbacks to recovery. Meanwhile, the European Union (EU)'s disbursement of the EUR 750 billion recovery fund should also provide additional fiscal support to the economy.

In contrast, China’s response to the COVID-19 pandemic has been measured, with more reliance on fiscal measures than large-scale credit loosening. To date, the monetary policy response has included liquidity injections, targeted cuts to banks' reserve requirement ratios, and modest reductions in the policy rate. Notably, China has fared better than most in successfully reopening its economy, hence reducing the need for policymakers to ease further. The broadening of the economic recovery to domestic consumption should also help.

In other parts of Asia, we have also witnessed policy rate cuts and fiscal stimuli, but in varying degrees. Wealthier nations have had more monetary and fiscal flexibility, in some cases to even indulge in quantitative easing (QE), without too many adverse consequences. As a result, budget deficits are rising, and we see limited room for more large-scale easing.

More broadly, COVID-19 has accelerated the pace of structural shifts in consumer behaviour, technological advancement and societal norms. Over and above keeping on top of these changes, there are several other key risks to take note of this year:

Read MoreFirstly, if the pandemic were to deteriorate further with no viable vaccine available, the respective governments will be forced to impose stringent lockdowns for longer, leading to much weaker-than-expected economic activities. In particular, countries with a heavy reliance on international trade, commodity exports, tourism and external loans will be disproportionately (negatively) affected by these developments.

Secondly, what started as a trade war between the U.S. and China is morphing into a struggle for supremacy within the high technology battlefield. It remains to be seen whether there will be a softening in foreign policy when the new Biden administration takes over. While U.S.-China tensions are unlikely to disappear, a more measured approach is expected under a Biden administration, and would undoubtedly be positive for global trade. In contrast, a re-escalation of the ‘technology war’ would be a major setback to trade and growth, with global and long-lasting ramifications.

Lastly, as the economic fallout from COVID-19 mounts, protests in emerging and frontier markets are set to swell with millions of unemployed, underpaid and underfed citizens. Long-standing grievances over socioeconomic inequalities, civil and political rights and government corruption could resurface, leading to domestic protests and riots that could hamper the pace of growth recovery.

| 2019 | 2020E | 2021E | |

|---|---|---|---|

| World | 2.8 | -4.1 | 4.9 |

| U.S. | 2.2 | -4.3 | 3.1 |

| Eurozone | 1.3 | -7.6 | 4.8 |

| Japan | 0.7 | -5.5 | 2.7 |

| China | 6.1 | 1.5 | 7.5 |

| ASEAN | 4.2 | -3.8 | 5.3 |

| 2019 | 2020E | 2021E | |

|---|---|---|---|

| World | 2.8 | 2.3 | 2.4 |

| U.S. | 1.8 | 1.2 | 1.8 |

| Eurozone | 1.2 | 0.3 | 0.9 |

| Japan | 0.5 | 0.1 | 0.2 |

| China | 2.9 | 2.8 | 2.0 |

| ASEAN | 2.0 | 1.2 | 2.0 |

| 1Q21E | 2Q21E | 3Q21E | 4Q21E | |

|---|---|---|---|---|

| Fed Fund Target (Upper band) | 0.25 | 0.25 | 0.25 | 0.25 |

| Fed Fund Target (Lower band) | 0.00 | 0.00 | 0.00 | 0.00 |

| ECB Deposit Rate | -0.50 | -0.50 | -0.50 | -0.50 |

| BOE Bank Rate | 0.10 | 0.10 | 0.10 | 0.10 |

| BOJ Target Rate | -0.10 | -0.10 | -0.10 | -0.10 |

Sources: Maybank Kim Eng, Bloomberg I November 2020

Source: Bloomberg I November 2020

Source: World Economic Outlook I October 2020